Updated: 25 Feb 2026

Upon securing a judgement against a debtor in Malaysia, Singaporean creditors can pursue a variety of additional legal debt enforcement methods if the latter continues to be delinquent.

Unfortunately none of them are this funny.

This variety exists for a reason - each facilitates recovery differently and varies in effectiveness depending on factors like:

-

type of debtor (business vs individual)

-

debtor’s motivation (legitimate dispute vs simply stubborn)

-

type of assets (cash or non-cash)

-

level of visibility into debtor’s net worth

And that’s just to name a few!

In representing clients, debt recovery lawyers appraise the facts of the case to determine the method with the best chance of recovery, and below, our friends at Rule & Co in Malaysia have prepared a list of six main court-ordered debt enforcement methods in Malaysia and when each works best.

Let’s begin.

Garnishee order

When it works best: If a debtor is known to hold significant cash assets

A garnishee order under Order 49 of the Rules of Court 2012 allows a creditor to directly collect (or ‘garnish’) money owed to the debtor by third parties such as clients, tenants, employers and especially banks holding the debtor’s accounts.

Briefly, it is a three-stage process:

-

Ex-parte application to freeze specific assets

-

Inter-parte hearing where the debtor can raise arguments, and

-

Granting of a Garnishee Order Absolute

Upon the granting of an Order Absolute, the third party (known as garnishees) will be legally compelled to release funds under their control directly to the creditor.

For more, this guide to garnishee orders in Malaysia explains which sources cannot typically be garnished as well as key limitations when attempting to garnish a bank account.

Writ of seizure & sale (WSS)

When it works best: If the debtor owns valuable non-cash assets

A writ of seizure and sale (WSS) under Order 47 of the Rules of Court 2012 empowers the court bailiff to seize the debtor’s movable and immovable property to satisfy a judgment debt.

While immovable property largely applies to just land or real estate, the list of seizable movable property is quite comprehensive and includes vehicles, machinery, office equipment, furniture, and product stock, and more.

Where it concerns movable property, a WSS has three main stages:

-

Ex-parte WSS application

-

Seizure of property by the court bailiff, and

-

Public auction and proceeds distribution

Crucially, debtors have a grace period to settle their debt before the auction and have their assets returned, so where the loss of said assets costs more than paying the debt, a WSS can be a powerful tool to secure recovery.

Immovable property is handled differently, and this Malaysian WSS guide covers it in full.

Judgment debtor summons (JDS)

When it works best: If the debtor’s financial position is unclear

A judgment debtor summons (JDS) orders the debtor to attend court to disclose, under oath, their financial means and reasons for disobeying the initial court ordered payment.

Where we lack visibility into the debtor’s assets, a JDS acts as a discovery tool with which we can confidently pursue more direct recovery methods like garnishee orders and writs of seizures.

In fact, this guide to judgement debtor summons in Malaysia explains how a debtor not showing up at the hearing can be used to apply one of the most painful debt enforcement methods of all!

Committal proceedings

When it works best: If there is proven disobedience of court orders by debtor

Committal proceedings under Order 52 of the Rules of Court 2012 can be used where a debtor has wilfully refused to comply with court-ordered payment, disclosure, attendance, or injunctions prohibiting the deposing of funds and assets.

If found in contempt, the debtor may be imprisoned for up to six weeks, and if they still defy the court order after release, a new committal petition may be brought against them!

However, the severity means it’s usually only granted as a last resort for the most stubborn debtors, and our committal proceeding guide explains how the courts typically decide.

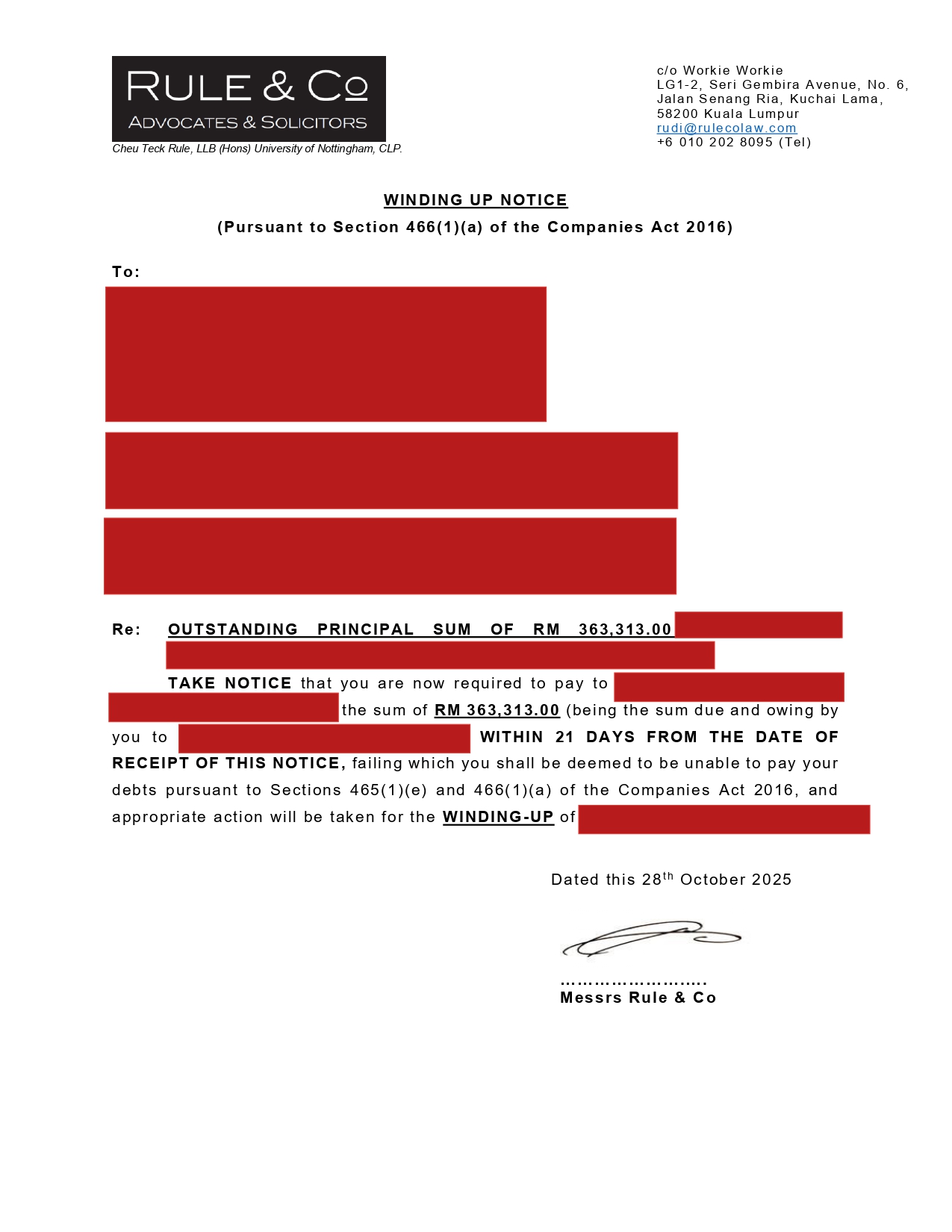

Compulsory winding-up / statutory demand

When it works best: If the debtor is an active, revenue-generating company; and not a “shell” company.

A creditor’s winding-up petition is a corporate insolvency mechanism used to indirectly compel payment by threatening compulsory liquidation of a debtor company via service of a statutory demand.

Upon service, the debtor company has 21 days to settle the debt before the creditor may file for a winding up petition, and most solvent companies will settle within this period to avoid liquidation.

For most unsecured creditors, this is the only desirable outcome, as should the company actually be liquidated, the order of proceeds distribution means little chance of a worthwhile recovery.

Bankruptcy proceedings / notice

When it works best: For individual debtors with means but unwilling to pay

A bankruptcy petition is the individual debtor’s equivalent of a winding-up petition and may be commenced where a debtor owes RM100,000 or more.

The debtor is served a bankruptcy notice giving them seven days to settle the debt, failing which they will have committed an Act of Bankruptcy (AOB) which entitles the creditor to begin bankruptcy proceedings against them.

Again, the goal is not to actually bankrupt a debtor, but for the threat of bankruptcy to compel repayment.

Don’t get stuck with an unenforceable court order

Pursuing any of the recovery methods above means three things:

-

filing a civil suit

-

winning a civil suit, and

-

the debtor still not paying!

Getting to this stage is never a good thing, as it likely means the debtor was never able to pay and the matter should never have been taken to court.

Over the years, we’ve been approached by innumerable creditors who assumed a civil suit was a surefire path to recovery and had in their hands a court order that was nothing more than a paper judgement.

They’d won their case, the debtor still refused to pay, and their lawyer informed them (after months and tens of thousands of Ringgit in legal fees) there was nothing more to be done.

Reasonable and solvent debtors don’t need a court to tell them to pay, and we welcome readers to get in touch for a free case assessment from our team.

That’s it from us, and we wish you a smooth debt recovery.